Introduction

“I like how you’ve brought out the rising popularity of UPI. I laud my fellow Indians for embracing digital payments! They’ve shown remarkable adaptability to tech and innovation”

Shri Narendra Modi, Hon’ble PM

Today, in India real time online payments have become very simple and easy. Few years ago, no one could have imagined that transferring amounts ranging from INR 1 to INR 100,000 (or even more) would become so simple. India tops in the list of countries with real payment apps in terms of volume i.e. number of transactions per day. Today, with the help of UPI these transactions have become very simple.

The importance of UPI was highlighted during the tough period of COVID-19 pandemic. When the country was under lockdown and cashless transactions were necessary UPI payment proved to be a lifeline for small and micro merchants.

In recent years UPI has emerged as one of the most important ways of carrying out transactions in India. The volume of UPI used in terms of transactions and the value have grown exponentially.Countries like France, Singapore etc. have started accepting the UPI as a method of payment.

In this article we will discuss what is UPI? How does it work? And also see the data related to the UPI. We will also compare it with other digital payment methods, which were used prior to the UPI.

What is UPI?

Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments into one hood. It also caters to the “Peer to Peer” collect request which can be scheduled and paid as per requirement and convenience.

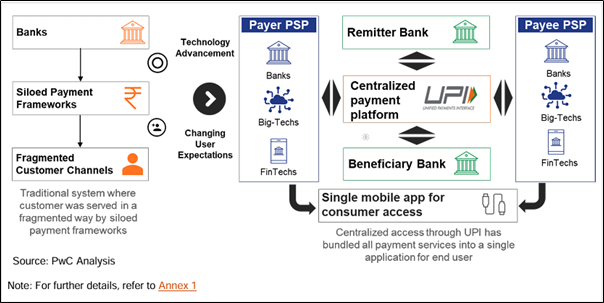

As said earlier UPI is centralized. Therefore any transaction request initiated through any third party payment channel passes through UPI. As the image below shows each user accesses UPI by a third party payment app. These apps are connected to the user’s bank account or multiple bank accounts. When the remitter scans any UPI supported QR, generated on any valid third party payment app used by the beneficiary the transaction is possible. If the user is not connected to UPI then, transaction across multiple apps is not possible.

Economic Survey 2022-23

http://cashlessindia.gov.in/upi.html

Background of UPI

Unified Payment Interface (UPI) was launched on 11th April 2016 by then Governor of RBI Dr. Raghuram Rajan & National Payments Corporation of India (NPCI). Banks had started to upload their UPI enabled Apps on Google Play store from 25th August, 2016 onwards. Prior to UPI, there existed other forms of cashless transactions such as internet banking and some other forms making banking easier.

Today, India has become one of the largest users of online payments, beating China (The Times of India, 2023). UPI has made retail transactions easier and convenient to carry out. UPI users are mainly mobile and internet users. As per some media reports (Business Standard, 2022) the number of mobile users in India, in 202, were 1.2 billion of which 750 million were smartphone users. This number is expected to reach 1 billion users by 2026. Increase in the number of smartphone users has led to the increase in online transactions. From the launch in 2016 the UPI transactions have increased year by year in terms of value as well as volume. Decision of demonetizing currency notes valuing Rs. 500 and Rs. 1000 accelerated the use of UPI.

When a customer needs to pay a small amount for day-to-day life, people usually rely on currency notes, coins. Earlier In the case of digital or cashless payments, people used to rely on card payments, but it wasn’t as easy as UPI. Moreover, card payments were majorly confined to higher amounts e.g. payment of restaurant bills, booking railway or air tickets etc. It wasn’t very popular in small transaction segments e.g. paying money to buy notebooks in a stationary shop. Prior to UPI, Paytm and other mobile banking service providers were operational, but their transactions had limited number of users. Few years back (before the introduction of UPI and common QR) paying through Paytm to a non-Paytm user was not possible. People were required to share bank account details to transfer the money. All these hurdles were removed after the introduction of UPI & the digital payments boom after the development of the common QR system.

UPI & other digital payment: comparison

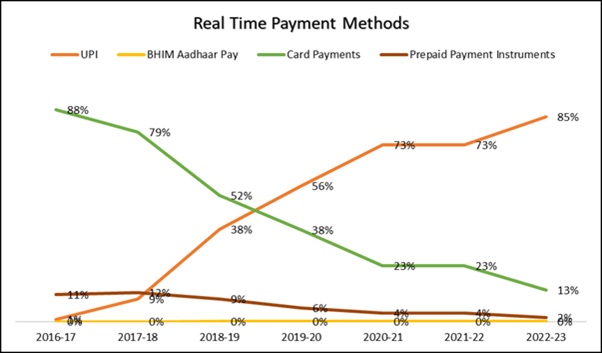

We will see a comparison between various types of cashless payments. The data used for the comparison of UPI, BHIM Aadhar Pay, Card Payment & Prepaid Payment Instruments is taken from the “Handbook of Statistics on Indian Economy” published by the Reserve Bank of India (RBI) annually. The card payments include both credit and debit cards used at the point of sales machine. The transactions carried to get cash from ATMs is not included. Another type of payment included for comparison is Prepaid Payment Instruments (PPI) i.e. payments through smart cards, vouchers, membership cards etc.

The above graph shows the dramatic growth of UPI since its inception. It has drastically replaced the card payment and also the share of PPI has reduced from 2016. BHIM Aadhar never had significant share in the sphere of digital payments therefore, the percentage of share is zero.

UPI Data

Much of the consolidated data is available with the National Payments Corporation of India (NPCI). The data used has been made available in the public domain by NPCI.

There are mainly 3 types of transactions which have taken place

- Customer initiated transactions

- B2C transactions

- B2B transactions

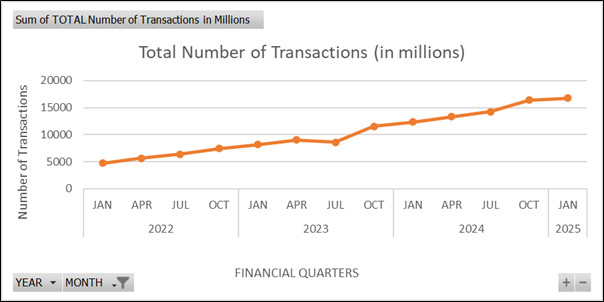

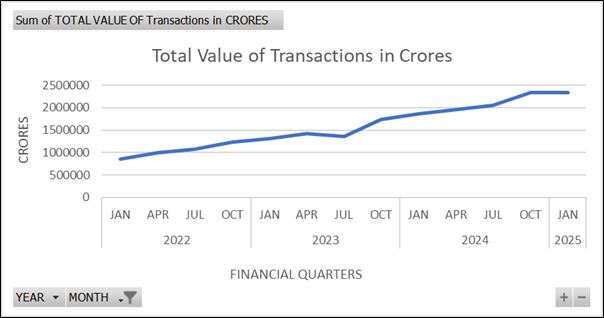

Following graphs shows the total value & volume of transactions carried out by using UPI.

In case of UPI payments, not only the volume of payments has exponentially increased but also the value of transactions has grown. Even after introduction in 2016, the number of transactions were around 5,000 in January 2022 which then raised to more than above 15,000 by July 2024, which is more than 3 times growth in the volume of users

The above graph depicts the growth in the value of transactions carried out through UPI. Over the time period of January 2022 to January 2025 this growth is around 175%! We have compared earlier that the rise of UPI payments has caused the decrease of the other payment methods.

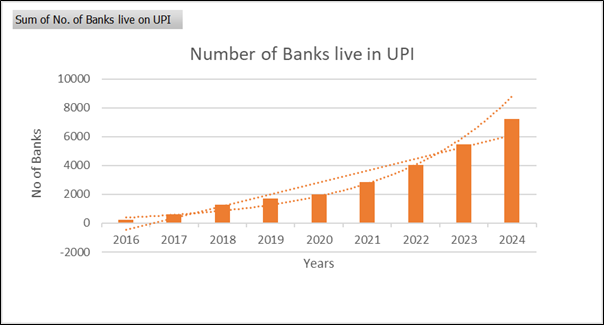

The growth in the UPI coincided with the growth in the number of banks associated with UPI. Back in 2016, when UPI was started there were only 221 banks providing UPI. Year-on-year this number has increased to 7,210 banks in 2024. UPI serving as a common platform for the payment/transactions & reducing hassles for the common users has been important for generating more demand from the people.

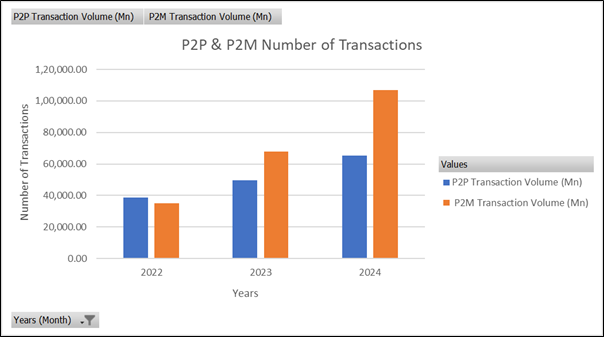

The following graphs depicts the picture of P2P & P2M transactions wherein:

- P2P- payments done by person to person

- P2M- payments done by person to merchant

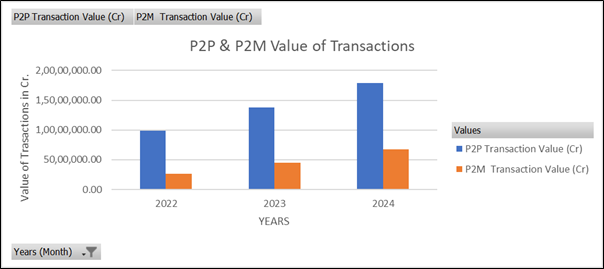

The graph shows the comparison of P2P and P2M transactions based on the total number of transactions. As we can see, the P2M number of transactions has increased by around 459% from 2022 to 2024. While on the other hand, the P2P number of transactions has increased by 129% during the same period. However, when we take a look at the value of transactions, it shows a different story. The graph below shows the value of transactions between P2P & P2M.

Earlier where we saw that the P2M transactions were more than P2P in terms of number of transactions, here value of P2P transactions has always remained high. In the year 2022, the total value of P2P transactions by UPI was around INR 99,12,336 Cr compared to P2M value of transactions which is INR 26,82,741 Cr. In the year 2024 it grew to INR 1,79,02,288 Cr and INR 67,80,232 Cr respectively. It highlights that the growth of P2P value of transactions was 153% and P2M was 283%.

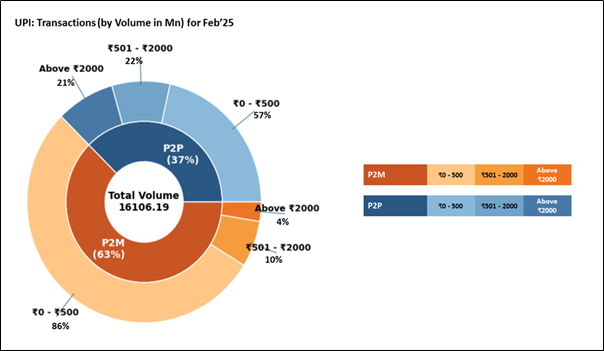

We have seen the expenses done through UPI, but there is a pattern even in the value of transactions carried out by Indians via UPI.

Earlier we have seen that, P2M transactions carried out through UPI were more that P2P transactions. As per the latest February 2025 figures, the share of P2M transactions was 63% whereas, the share of P2P transactions was 37%. Further, we can also see that in both the spheres the share of small transactions i.e. from INR 0- INR 500 is the most. In P2M it contributes up to 86% and in P2P it contributes to 57%. This actually highlights that the common people of India are using UPI as their regular method of transaction instead of cash.

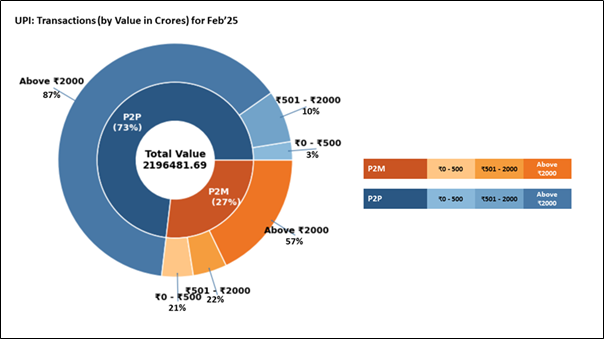

Similar is the scenario for the value of transactions. However, here P2M transaction share is lesser than P2P transactions. The total share of P2P transactions is 73% & P2M share is just 27%. When we go further in detail, we see that the large value transactions occupy the space. Transactions valued more that INR 2000 contribute to 87% in P2P sphere and 57% in P2M share. As opposed to earlier graph, low value transactions of INR 0- 500 are only 10% & 21% in P2P & P2M sections respectively.

In the year 2022, Bengaluru topped the list of most transactions through UPI. The city recorded 29 million transactions worth INR6500 crore in 2022. Second on the list is Delhi which amounted to 19.6 million transactions worth INR5000 crore followed by Mumbai with 18.7 million transactions worth INR4950 crore. On number 4 is Pune with 15 million digital transactions worth INR3280 crore and Chennai with 14.3 million transactions worth INR3,550 crore. This highlights the acceptance of the UPI in India. (The mint, 2023)

Why UPI is special

The NPCI has explained how UPI is unique. It is as follows:

- Immediate money transfer through mobile device round the clock 24*7 and 365 days.

- Single mobile application for accessing different bank accounts.

- Single Click 2 Factor Authentication – Aligned with the Regulatory guidelines, yet provides for a very strong feature of seamless single click payment.

- Virtual address of the customer for Pull & Push provides for incremental security with the customer not required to enter the details such as Card no, Account number; IFSC etc.

- QR Code

- Best answer to Cash on Delivery hassle, running to an ATM or rendering exact amount.

- Merchant Payment with Single Application or In-App Payments.

- Utility Bill Payments, Over the Counter Payments, QR Code (Scan and Pay) based payments.

- Donations, Collections, Disbursements Scalable.

- Raising Complaints from Mobile App directly.

Along with the above-mentioned benefits UPI transactions are fast and secure. That has created confidence within customers. It has also increased the convenience for customers as well as retailers.

UPI outside of India

These benefits of UPI have made it popular very quickly, not only in India but also in India. As per media report of mintgenie of 18th July 2023, along with Bhutan, Oman, Malaysia, Thailand, Philippines, Vietnam, Singapore, Cambodia, South Korea, Japan, Taiwan, Hong Kong, United Kingdom, Nepal and France had accepted UPI (Team MintGenie, 2023).

UPI also took centre stage during the G-20 conference. In the G20 conference India provided hands-on-experience of using UPI. SBI, Axis Bank, Canara Bank and ICICI bank launched dedicated UPI with a balance of INR 2000 for delegates to buy goods by QR scanning and experience the usage of UPI. (Singh, 2023)

NPCI has also launched “UPI One World” for foreign nationals and NRIs. It is the Prepaid payment instrument linked to UPI provided to foreign nationals/ NRIs coming from G20 countries. Foreign nationals and NRIs from G-20 nations with the help of minimum KYC (valid visa and passport) registrations can enjoy UPI. Customers of PPI-UPI can charge UPI valet against receipt of foreign exchange by cash or any payment instrument. Then the customer can use the PPI-UPI app as regular UPI users, through scanning QR code at UPI enabled merchants. This will promote the cashless transactions as well as save the hassles of carrying cash.

UPI has brought a revolution in the cashless payment system. Even a minister form Germany was amazed by the ease of transaction through UPI. UPI has also adopted changes for the better experiences for NRIs and foreign nationals. Along with these developments RBI is continuously running a campaign for the awareness about the UPI to secure customers from frauds. In the near future we can expect more and more growth in UPI based cashless transactions.

UPI & Digital Rupee

Digital rupee pilot programme was launched in December 2022. In September 2023, NPCI issued a notification to all the users of UPI that the benefits of the QR code would be extended to the Digital Rupee also. This decision has been taken in line with Reserve Bank of India’s (RBI) decision of enhancing CBDC and UPI interoperability. This interoperability will allow users of retail digital rupee to make transactions by scanning the QR code and allow merchants to accept the digital rupee. Currently, there are 15 banks offering Central Bank Digital Currency (CBDC) wallet. These are:

- State Bank of India

- ICICI Bank

- IDFC First Bank

- Yes Bank

- HDFC Bank

- Union Bank of India

- Bank of Baroda

- Kotak Mahindra Bank

- Canara Bank

- Axis Bank

- Indusind Bank

- PNB

- Federal Bank

- Karnataka Bank

- Indian Bank

The UPI has become very handy instrument for the transactions. The exponential growth of UPI shows its success. It has revolutionised the way of monetary transactions so much so, that the developed nations like France have also started accepting UPI.

References

Business Standard. (2022, January 3). India to have 1 billion smartphone users by 2026: Deloitte report. Business Standard. Mumbai, Maharashtra, India: Business Standard Private Limited (BSL). Retrieved from https://www.business-standard.com/article/current-affairs/india-to-have-1-billion-smartphone-users-by-2026-deloitte-report-122022200996_1.html

Singh, S. (2023, September 9). Hello UPI: Digital payment apps take center stage at Delhi G20 Summit. INDIA TODAY. Retrieved from https://www.indiatoday.in/diu/story/upi-digital-payment-apps-take-center-stage-at-delhi-g20-summit-2433518-2023-09-09

Team MintGenie. (2023, July 18). UPI in France: List of countries that adopted India's payment system. HT Digital Stream Ltd. HT Digital Stream Ltd. Retrieved from https://mintgenie.livemint.com/news/personal-finance/upi-in-france-list-of-countries-that-adopted-indias-payment-system-151689599406411

The mint. (2023, April 18). India saw record of ₹149.5 trillion UPI, card transactions in 2022; THIS city tops the list. HT Media Group. Retrieved from https://www.livemint.com/news/india/india-saw-record-of-rs-149-5-trillion-upi-card-transactions-in-2022-this-city-tops-the-list-11681789465771.html

The Times of India. (2023, June 12). India tops world ranking in digital payments, beats China by huge margine: Report. The Times of India. Mumbai, Maharashtra, India: Bennett, Coleman & Co. Ltd. (B.C.C.L.). Retrieved from https://timesofindia.indiatimes.com/gadgets-news/india-tops-world-ranking-in-digital-payments-beats-china-by-huge-margin-report/articleshow/100944643.cms

https://www.rbi.org.in/commonman/English/scripts/FAQs.aspx?Id=3686